Eight major industrial software powers in the world

Most of the top software in the world, such as CAD and CAE, are in the hands of European and American countries. When it comes to CAD, many people think it is Autodesk’s AutoCAD. In fact, besides Autodesk in the United States, Dassault in France, Siemens in Germany, and PTC in the United States are all leading companies in CAD, and these four companies account for more than 90% of their domestic CAD market share. It is worth mentioning that Ansys, Altair, and MSC have basically monopolized the CAE field.

According to data from 2020, the global industrial software market reached a size of 435.8 billion US dollars. Especially the three giants of EDA software, Cadence (Kaiden Electronics, USA), Synopsys (New Thinking Technology, USA), and Mentor (Mingdao Electronics, a subsidiary of Siemens, Germany), occupy 90% of the global market share, and their market share in China has reached 95%.

Industrial software refers to software specifically designed for the industrial field, including systems, applications, middleware, embedded systems, etc. Industrial software is generally divided into two types: embedded software and non embedded software. Embedded software refers to software embedded in controllers, communication, and sensing devices for data acquisition, control, and communication; Non embedded software refers to design, programming, process, monitoring, management, and other software installed in general-purpose computers or industrial control computers. Especially embedded software, applied in fields such as military electronics and industrial control, has particularly high requirements for reliability, safety, and real-time performance. It must undergo strict inspection and evaluation, and special emphasis should be placed on software related to design.

Industrial software plays a very important role in product design, complete equipment design, plant design, and industrial system design. It can greatly improve the level of research and development, manufacturing, and production management of industrial enterprises, improve industrial management performance and design efficiency, effectively save costs, and achieve visual management. It is the “brain” of modern industrial equipment, and also a powerful weapon for manufacturing industry to implement industrial Internet and transform intelligent manufacturing. The following are the eight major industrial software powers in the world:

1、 United States

The United States is one of the world’s leading countries in industrial software. In fact, the largest industrial software company in the United States is Lockheed Martin. In the 1960s, hand drawn drawings could no longer meet the increasingly complex product demands, and aerospace giants such as Boeing, Lockheed, and NASA began developing industrial software to replace manual drawing. Because computer technology can better express product requirements and eliminate the need for manually driven physical equipment.

Especially during the Cold War, in order to reduce expensive military software expenditures and promote military civilian integration, Lockheed Corporation seized the opportunity to enter the industrial software field. It is worth mentioning that the industrial software developed during this period was all for enterprise use. Later, in order to earn profits, many software were converted into commercial use. Currently, CADAM, developed by Dassault Systema and invested by Lockheed, is still active in the market; UG developed by McDonnell Douglas, ANSYS developed by Westinghouse Electric Space Nuclear Laboratory, and so on.

The United States attaches great importance to the development of software and industrial software. For example, NASA, in collaboration with companies such as GE and Pratt&Whitney, has developed the NPSS software over a period of 20 years, which embeds a large amount of engine design knowledge, methods, and technical parameters. It can complete a round of aircraft engine design within one day. For example, the entire development process of the Boeing 787 used over 8000 industrial software, of which less than 1000 were commercial software, while the remaining over 7000 were proprietary software accumulated by Boeing over the years and not sold to the public, including Boeing’s core engineering technology.

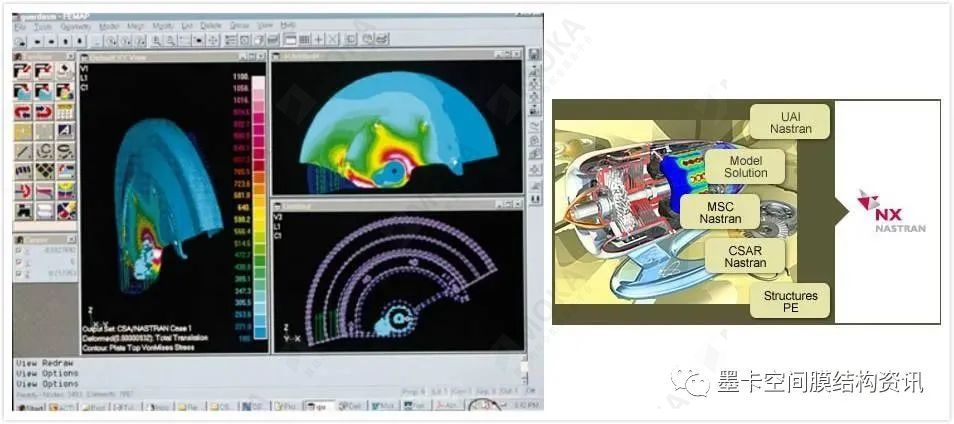

Industrial software is the foundation of future strategic emerging industries. Without industrial software, intelligent manufacturing would be a pipe dream. Today, almost every industrial product in the world is an important crystallization of industrial software. The United States is the earliest country in the world to develop CAE, and it started with NASA. With the support of national funds, NASA has developed the famous finite element analysis software Nastran. In 1971, MSC improved the Nastran program, thus becoming the pioneer of simulation software in the United States.

2、 Germany

The German software industry is the leader in the European software industry, with the highest number of customers and manufacturers among EU countries. From a global perspective, Germany has also maintained its position as one of the world’s largest software suppliers and solution providers. The software industry is an important component of Germany’s information and communication technology (ICT) industry. There are over 30000 companies in Germany specializing in software development and sales in the basic software industry, which used to account for about 46% of the total number of companies in the ICT industry.

The characteristic of Germany’s major software companies is that they are “young”, with 67% of them established in the 1990s, most of which are new companies that stand out from universities, research institutions, and large enterprises. According to relevant information, the exports of major software companies in Germany are mainly from EU countries, while the export focus of auxiliary software companies is on North American and Asian countries.

From the perspective of software development methods, major software companies and auxiliary software companies in Germany have their own distinct characteristics in software development. 73% of major software companies are engaged in independently developing original software, while 87% of auxiliary software companies purchase basic software and improve it for their own use. According to statistics, 2/3 of the software used by auxiliary software companies is standard software.

The German government attaches great importance to the encouragement policies of the IT industry, believing that the development of the IT industry has important strategic significance for the country’s economic and social development. The development status of the IT industry determines the external competitiveness of the German economy, determines whether the German economy can sustainably develop, and determines whether Germany can have sufficient labor employment opportunities in the future. To encourage the development of the IT industry, the German government has introduced a series of policy measures at different levels, including the “Information and Communication Technology 2020- Research for Innovation” plan, the “Innovation and Employment in the 21st Century Information Society” action plan, the “Information Society Germany 2006” action plan, the “Information Society Germany 2010” action plan, the “Everyone uses the Internet” ten point plan, the “IT for Education: Don’t Stop Going Online” action plan, the “Multimedia” plan, and the “Small and Medium sized Enterprise Information and Communication Technology Innovation Offensive” encouragement measures.

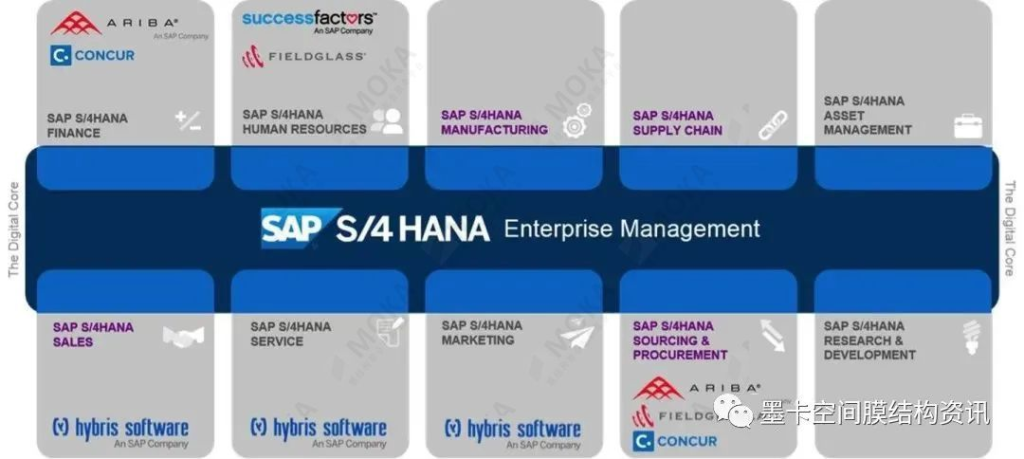

The largest industrial software company in Germany is SAP SE. Although only a software company, it is a company leading Germany’s “Industry 4.0” strategy. SAP is the world’s largest provider of enterprise management and collaborative e-commerce solutions, and the third largest independent software supplier globally. SAP is also the world’s largest supplier of business applications, enterprise resource planning (ERP) solutions, and independent software, with a market share of over 30% in global enterprise application software. It is worth mentioning that over 80% of the Fortune 500 companies are using SAP’s management solutions. Since 1988, SAP has been listed on multiple stock exchanges, including the Frankfurt Stock Exchange and the New York Stock Exchange.

Although SAP used to rank only over 400 in the previous Fortune 500, 80% of the companies in the Fortune 500 were its customers. Industry 4.0 “is a highly automated, digitized, and networked intelligent manufacturing model centered around Cyber Physical Systems (CPS) and utilizing three integrations (vertical integration, end-to-end integration, and horizontal integration) to achieve efficient, agile, and intelligent production, resulting in a qualitative leap in efficiency, cost, quality, and personalization.

In addition, FAUSER Corporation, established in 1994, is a top global APS (Advanced Scheduling System) software company, with its products positioned as intelligent planning and scheduling for Industry 4.0. FAUSER’s product chassis numbers are widely used by thousands of companies such as Lockheed Martin in the United States, BAE Systems in the United Kingdom, Airbus, BMW, DaimlerChrysler, ThyssenKrupp, Kohler Sanitary Ware, etc., becoming the command system for these companies’ “intelligent manufacturing”.

Another well-known German giant, Siemens, is also one of the world’s largest industrial software giants and a leading automation giant. Siemens once manufactured the world’s first 800kV ultra-high voltage direct current transformer, which became the core device for ultra-high voltage transmission. Siemens provides automation systems and PVSS construction solutions for the world’s largest particle accelerator, the European Large Hadron Collider, and is the only industrial development and sponsor of the European Large Hadron Collider project.

3、 Japan

As the world’s third-largest economy, Japan used to be second only to the United States in software sales, with outstanding embedded software capabilities. Even independent research institutions rank Japanese software quality and productivity far above that of the United States. However, Japan’s software products and services still lack a global presence, mainly due to the huge gap between its strong software development process capabilities and weak product innovation capabilities.

Most Japanese IT companies are located in industries with low software intensity. The reason why the US software industry is superior to Japan is due to its first mover advantage, which is driven by the US research and development policies and the leading development of computer science education at the university level, and its advantages continue to this day. For example, one-fifth of software developers in the United States have received graduate education, while only one tenth in Japan. The gap in doctoral degrees is even greater. But it is worth mentioning that the global software outsourcing market has reached a scale of 100 billion US dollars, with Japan alone accounting for one tenth.

Although Japan does not have a thriving and comprehensive industrial software industry, it has made significant achievements in certain software fields. Japanese companies focus on the development of embedded software. For example, CNC machine tools, intelligent robots, and automobiles are the three major carriers of embedded software in Japan.

In fact, almost all devices in Japan with digital interfaces, such as watches, microwave ovens, mobile phones, digital TVs, cars, etc., use embedded systems, and embedded software covers a wide range of fields. So, these are enough to make Japan dominate the world in tiny and sophisticated electronic products for decades. However, the development of a distorted industrial software system cannot provide long-term protection for Japan’s manufacturing industry, which is also the reason why Japan’s manufacturing industry has shown a significant downward trend in recent years.

4、 France

France is one of the industrial software powerhouses. Ranked fifth after the United States, Japan, Germany, and the United Kingdom. As early as February 2012, France released “Digital France 2020”, which includes three main themes: developing fixed and mobile broadband, promoting digital applications and services, and supporting the development of electronic information enterprises. In France, the software industry has always been regarded as the “locomotive” of the national economy. Especially in September 2013, French President Hollande announced the “New Industrial France” strategic plan, hoping to promote employment through industrial innovation and growth in the next decade, boost the competitiveness of French enterprises, and make France’s competitiveness at the forefront of the world. The “New Industrial France” plan includes 34 initiatives covering various fields such as digital technology (including embedded software and system plans, big data plans, and cloud computing plans), energy, transportation, smart grids, nanotechnology, healthcare, and biotechnology.

Most French software companies are small and medium-sized enterprises, with 70% of them having an annual turnover of less than 10 million euros. The internationalization level of the French software industry is not high, with only about 23% of its revenue coming from foreign markets, of which 14% comes from the European market. In recent years, France has rapidly become one of the world’s important providers of service outsourcing. The outsourcing rate of French software service companies once reached 63%.

The globally renowned industrial software giant, Dassault Systemes from France, was once the world’s largest industrial software provider. Dassault Systemes’ presence has already appeared in many well-known projects around the world, such as the Bird’s Nest Stadium, Beijing Xiongnu High speed Railway, Daxing Airport, C919 aircraft, Haixun 160, etc. It has also provided comprehensive solutions for the Shanghai World Expo. Dassault Systemes has a complete set of PLM software, providing software system services and technical support for various industries including aviation, automotive, and mechanical electronics. Dassault Syst è mes was founded in 1981 and is headquartered in Paris, France. Dassault Syst è mes has always been a pioneer in global 3D software.

Dassault’s flagship product CATIA integrates 2D and 3D functions. The powerful functionality of this software has made it a leading global automotive design application and a leading aviation design application, even making Boeing a stable customer. In the 1990s, Dassault Systeme established a subsidiary in Japan to further expand its global market.

5、 Canada

Canada is a global traditional software powerhouse. Canada has many famous software companies, such as OpenText, Corel Multimedia Office Suite, Houdini 3D Animation Software, Solido Design Semiconductor Design, and various 2B software companies such as Fintech. It is worth mentioning that Canada’s overall development level and strength in basic software and industrial software are second only to the United States, France, and Germany.

Especially, most of Canada’s basic and industrial software are world firsts. For example, Canada’s outstanding power and oil professional simulation software CMG suite, CYME, PSCAD, almost monopolize the software market worldwide. Canada also has a large number of media office software, semiconductor design, 3D animation software and other world-class companies.

6、 United Kingdom

The annual revenue of the UK’s electronics industry used to rank fifth in the world. Electronic companies are mainly distributed in the eastern region of England, Wales, and Scotland. Scotland is the main production base and is known as the ‘Silicon Valley’. World renowned computer manufacturing companies such as IBM, Compaq, Sun, ICL, and PSION have established factories in the UK, making it the largest computer production country in Europe.

The service industry in the UK accounts for 70% of its GDP, of which 70% comes from information technology services. The development speed of software in the UK far exceeds the average level of economic development. At present, the software and information services industry in the UK has surpassed the electronics industry. The UK has world-class universities and research institutions with strong software development capabilities. Many international information technology conglomerates have established research and development centers in the UK, such as Computer Associate and Microsoft.

In addition, British companies attach great importance to research and development investment. According to the latest statistics from the UK Office for National Statistics, pharmaceutical, aviation, electronics, and communication companies rank among the top three in terms of R&D expenditure among all UK enterprises. It is worth mentioning that the UK market once accounted for approximately 20.3% of the entire European IT market and 5.8% of the world IT market. In the UK computer industry market, computer services account for the largest proportion, followed by hardware, software, and networking.

7、 Ireland

Ireland was previously known as the ‘European countryside’, but since 1994, its GDP has maintained a high growth rate of around 9%, especially reaching 10.5% in 2000, ranking first among all European countries. Especially, the Irish computer software industry has emerged as a rising force, achieving remarkable global competitiveness in the software field.

According to a research report released by the OECD (Organization for Economic Cooperation and Development), Ireland once surpassed the United States to become the world’s largest software exporting country. Currently, 43% of computers and 60% of supporting software in the European market are produced in Ireland. As a result, Ireland has earned accolades such as the “Celtic Tiger,” “European Software Capital,” “New Silicon Valley,” “Software Kingdom,” “Dynamic High Tech Nation,” and “European High Tech Center.

The beginning and development of the Irish software industry, which used to be the “European countryside” and is now the “capital of software”, roughly went through three stages: the slow start stage (1970-1985), mainly using foreign software products to provide services to users, while also producing some products, but with lower profits; During the steady development stage (1986-1995), the domestic software industry gradually developed into an emerging industry and began to sell to the international market; During the high-speed development stage (1996 present), software companies began to go public and merge.

Ireland is the headquarters of companies such as Motorola, IBM, INTER, LOTUS, etc. in the European Union. Seven of the world’s top 10 software companies have factories in Ireland, and some have even established research and development centers. The software industry has become a pillar industry for the development of the Irish national economy, such as the famous Intel Quark chip designed in Ireland.

8、 India

India is a world-renowned software powerhouse. In the 1960s, the ‘father of software in India’, Koli, introduced the concept of software to India. A significant proportion of India’s population is illiterate, but at the same time it has 410000 software technicians, and this number is still growing.

It is worth mentioning that there are 1832 educational research institutions and polytechnics in India, which train approximately 70000 computer software professionals annually. Currently in the United States, one-third of software engineers are Indian, and it is surprising that 250000 people are deeply involved in Silicon Valley. Some people metaphorically say that India relies on the top 2% of elites at the top of the pyramid to drive 98% of the civilian population. No wonder Bill Gates asserted after his first visit to India that India has the potential to become a software superpower in the coming years.

The successful application of export strategies in the software industry is an important link for India’s software industry to go global. There are two main export strategies for the development of the software industry in India. One is the so-called “onshore service”, which involves Indian software companies sending engineers to work with foreign clients and ultimately completing designs; The second is the so-called ‘offshore service’, which refers to completing software program development in India, transmitting it to the client for testing and installation. These two businesses once accounted for 57% and 35% of India’s software output value, respectively. It is worth mentioning that India mainly provides customized software services, with a small proportion of branded suite software. Therefore, India’s software industry model belongs to “software outsourcing”.

Top 100 global software companies and their respective countries

(Comprehensive strength ranking for reference only)